Support the Timberjay by making a donation.

Groups seek closer look at PolyMet viability

Environmentalists question mine’s ability to fund required financial assurance

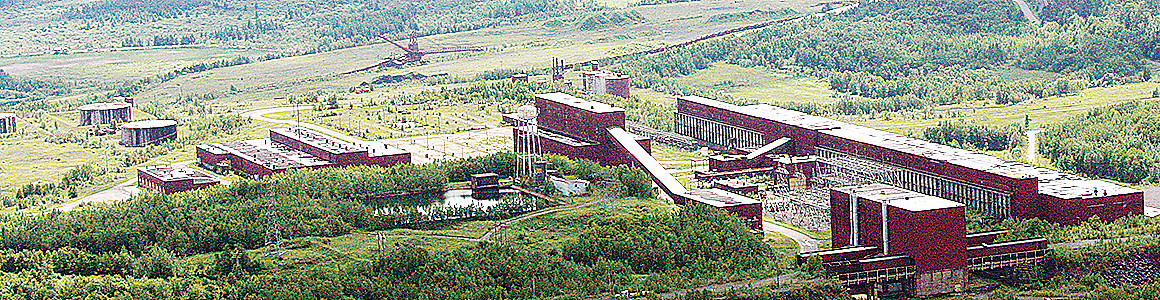

REGIONAL— PolyMet’s recently-updated feasibility study, or technical report, is prompting calls for a closer look by state regulators at the financial viability of the company’s proposed …

This item is available in full to subscribers.

Attention subscribers

To continue reading, you will need to either log in to your subscriber account, below, or purchase a new subscription.

Please log in to continue |

Groups seek closer look at PolyMet viability

Environmentalists question mine’s ability to fund required financial assurance

REGIONAL— PolyMet’s recently-updated feasibility study, or technical report, is prompting calls for a closer look by state regulators at the financial viability of the company’s proposed NorthMet mine and whether PolyMet’s principal financial backer, Glencore, should be assuming a larger role in the project.

Separate comments filed by the Minnesota Center for Environmental Advocacy and the Duluth-based Water Legacy, argue that profits generated by the mine, as currently envisioned, are unlikely to allow the company to meet the financial assurance obligations required to obtain a permit to mine from the Department of Natural Resources. And the groups cite evidence that suggests that PolyMet officials have known this for some time, even as they have maintained otherwise.

“The NorthMet mine project as proposed in the permit to mine application is clearly uneconomic, and will never be built in its current form,” wrote MCEA attorney Kevin Lee, in comments filed this week with the DNR. MCEA was joined in its comments by the Center for Biological Diversity and Friends of the Boundary Waters.

Both Water Legacy and MCEA recently submitted requests for a contested case proceeding on the project, and they want financial questions to be addressed as part of that examination. A contested case is overseen by an administrative law judge and is designed to resolve major factual disputes between parties short of an actual courtroom. The DNR has yet to decide if it will agree to such a proceeding.

PolyMet spokesperson Bruce Richardson questioned the need for such a process. “The environmental review and permitting process has been so comprehensive, we believe the agencies have all the information they need and are in the best position to make final permitting decisions.”

The latest push for a more in-depth financial inspection comes in the wake of PolyMet’s release its updated technical report, which showed substantially diminished financial returns on the project compared to a previous financial update released in 2012. The report also projected that the costs to build the mine have jumped significantly, from an earlier estimate of about $650 million to just over $945 million, to as much as $1.2 billion including the cost of a hydrometallurgical processing facility. But it is the internal return on that investment (IRR), of just 9.6 percent, that has caught the attention of critics of the project, as well as investors. PolyMet’s stock price has yet to recover from the slide it suffered in the immediate release of the new technical report. The stock was trading at 90 cents per share as of Tuesday afternoon.

“For a project as risky as a mine, investors typically demand much higher returns to justify the risk,” stated MCEA’s Lee in his comments. “For new projects, a 40-percent IRR is the target, and in general a 20-percent IRR is the minimum.”

Richardson said the company disagrees “emphatically” with the suggestion that the mine proposal is not financially viable, and he notes that the technical report points to $1.5 billion in project positive cash flow during the 20-year anticipated life of the mine.

Yet critics of the project suggest that the company’s cash flow projections are sugarcoated because they don’t include the company’s obligation to finance a long-term water treatment trust fund, currently expected to cost $580 million, which is included in the draft permit to mine.

Indeed, a cash flow model included in PolyMet’s updated technical report does not appear to include those required payments, which would run about $55 million annually beginning in the ninth year of mine operations. Richardson notes that the cash flow does include the cost of ongoing reclamation. Yet reclamation is just one part of the company’s obligation under the draft permit to mine. The cost of long-term maintenance and water treatment, which is expected to extend for centuries, is the largest expense, and it would be financed by a separate trust fund that PolyMet has proposed to finance through cash flow created by their mining operations.

Richardson said the anticipated cash flow from the mining operation is “more than enough” to finance the trust fund.

Yet, environmentalists aren’t the only ones to raise concerns about PolyMet’s ability to fund its financial assurance obligations. The DNR’s financial consultant, Emmons Olivier Resources, Inc., or EOR, has consistently raised concerns about PolyMet’s ability to finance its long-term water treatment obligations, given the uncertainty of the costs and the frequency with which small mining companies declare bankruptcy. And that was before the company issued its latest feasibility report, with its lower profit projections.

That view is bolstered by a May 4, 2017 email from a DNR consultant who tells DNR officials and others working on the project that PolyMet is unlikely to be able to obtain surety bonds on its own, which is one of the ways the DNR expects the company to finance its obligations. Don Sutton, an engineer with Montana-based Spectrum Engineering and Environmental, indicated he had spoken to a representative of the Surety and Fidelity Association of America, who told him that PolyMet would be unable to obtain surety bonding without Glencore backing the risk.” Glencore, based in Switzerland, is a massive international commodity brokerage that has been PolyMet’s chief financial backer to date. “Given the size of the bonds, the surety would only bond a company with many billions in assets. Glencore is in that class,” Sutton added.

PolyMet’s relatively limited assets is not just a concern to the surety industry. Water Legacy legal counsel Paula Maccabee argues in new comments that Glencore must be included in the permit to mine in order to protect taxpayers. She argues that Glencore is now so intertwined with PolyMet in terms of financing and governance, that it should be considered a party to the mining permit. “It may serve PolyMet’s and Glencore’s interests to propose that only PolyMet be deemed a permittee for a Permit to Mine,” wrote Maccabee in comments filed April 5. “However, Minnesota’s law supports and Minnesota’s public interest requires that no permit to mine for the NorthMet project be considered that does not include Glencore as one of the “persons” proposing to jointly engage in the proposed nonferrous mining operation.”

Glencore, based in Switzerland, has a significant ownership stake in PolyMet and options to purchase a larger share of the company. It has also been PolyMet’s chief financial backer through the development phase of the project and now has three representatives on the PolyMet board of directors. Glencore has also agreed to purchase 100 percent of the metal concentrates produced by the mine.

DNR officials say they have questions of their own following release of the technical report, and plan to have their financial consultant review PolyMet’s filing before issuing any permit to mine. ‘I do not have an estimate of when that review will be completed,” said Barb Naramore, DNR assistant commissioner.

The company would, in either case, have to demonstrate its ability to fund at least a sizable portion of its financial assurance obligations prior to begin mine excavation.

Bait and switch alleged

Environmental critics allege that PolyMet officials have known for some time that the mine proposal it was advocating would not be economically viable.

“The Applicant virtually conceded this in the Technical Report, and requested analysis of alternative mine designs at much higher throughputs, up to almost quadruple the current proposal,” states Lee in his comments. “The updated technical report is a staggering concession. What it makes clear is that if Minnesota ever sees a NorthMet project, it will be as a mega-mine processing four times as much rock as proposed today, and generating four times the waste, creating a tailings basin four times the size.”

Lee said the evidence suggests that PolyMet officials were aware that their mine plan was “economically marginal,” and he pointed to a 2013 economic analysis the company commissioned from Edison Investment Research that explored the economics of a 90,000 ton-per-day mine plan. “That report found that [PolyMet’s] share price would almost triple if the project were expanded to process much higher tonnages,” stated Lee. “At the time the report was commissioned, [PolyMet] denied plans for an expansion, saying “[t]hat’s not part of our discussions around here.”

Lee said denials by PolyMet that it was pursuing expansion plans “can now only be seen as misleading.”

PolyMet’s Richardson rejects that suggestion. “This is simply not true,” he said. “The permit applications we filed and the draft permits that have since been released are for a 32,000 tons-per-day operation. This is stated clearly in the technical report and all of our communications on the subject. We have been clear that any change in the mine plan would require additional engineering, environmental review and permitting.

”

Assurance plan complex, costly

Special conditions included in the DNR’s draft permit to mine would require PolyMet to put up $75 million at the start of construction, primarily to cover legacy costs from the former LTV mine. Ten million dollars of that would need to be in cash, with the rest potentially coming from surety bonds or irrevocable letters of credit.

By the first year of mining, the company would be required to post financial assurance totaling $588 million, which would cover the anticipated reclamation and long-term site management costs at that point. The company’s obligations would continue to grow until about the tenth of mining, when the financial assurance requirement would peak at just over $1 billion. That requirement would gradually decline as the company completed ongoing reclamation, but the company’s cash outlays for financial assurance are expected to jump sharply at Year Nine, to about $55 million a year, as the financial assurance fund transitions from an expected heavy initial reliance on bonds and letters of credit, to cash. Those are the payments that do not appear in the cash flow model included in PolyMet’s latest technical report.

Richardson notes that the cash flow does include the cost of ongoing reclamation, although it’s not clear how much the company is assuming since the reclamation costs in the cash flow are lumped with other unrelated costs. Yet reclamation is just one part of the company’s obligation under the draft permit to mine. The cost of long-term water treatment, which is expected to extend for centuries, is the largest expense, and it would be financed by a separate trust fund that PolyMet has proposed to finance through cash flow created by their mining operations.

While Richardson argues that the $1.5 billion in positive cash flow that the project is expected to generate will be sufficient to cover the long-term management costs, it’s unclear how including those costs would impact the company’s overall projected returns. When the Timberjay sought clarification on this issue, Richardson did not respond.

It appears that the company may be banking on lower long-term water treatment costs than initially thought. The company makes clear in its latest filing, that it assumes that the wild rice sulfate standard will be modified. The company had promised in the past to meet the wild rice standard, of ten milligrams per liter, but it now assumes that the standard will be changed or eliminated. Legislation advancing through the state Legislature this session, would, in fact, eliminate the standard, although environmental groups claim such a measure, if passed, would violate federal law and would likely be subject to litigation.

The DNR’s financial assurance calculations are based on the current sulfate rules, according to Naramore. She also notes that a change in the law could impact the financial requirements of long-term water treatment. “As you know, the cost of long term treatment is a large portion of the total financial assurance liabilities,” said Naramore. “So, it stands to reason that, if the sulfate standard changed, it could impact level of treatment required and thus treatment costs and financial assurance requirements. DNR has not, however, evaluated any financial assurance scenarios involving modified sulfate standards,” she added.